Abstract¶

This notebook explores multivariate relationships through linear regression analysis, highlighting its strengths and limitations. Practical examples and visualizations are provided to help users understand and apply these statistical concepts effectively.

Goals of this lecture¶

There are many ways to describe a distribution.

Here we will discuss:

Measurement of the relationship between distributions using linear, regression analysis.

Importing relevant libraries¶

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns ### importing seaborn

import pandas as pd

import scipy.stats as ss%matplotlib inline

%config InlineBackend.figure_format = 'retina'import pandas as pd

df_estate = pd.read_csv("data/models/real_estate.csv")

df_estate.head(5)Describing multivariate data with regression models¶

So far, we’ve been focusing on univariate and bivariate data: analysis.

What if we want to describe how two or more than two distributions relate to each other?

Let’s simplify variables’ names:

df_estate = df_estate.rename(columns={

'house age': 'house_age_years',

'house price of unit area': 'price_twd_msq',

'number of convenience stores': 'n_convenience',

'distance to the nearest MRT station': 'dist_to_mrt_m'

})

df_estate.head(5)We can also perform binning for “house_age_years”:

df_estate['house_age_cat'] = pd.cut(

df_estate['house_age_years'],

bins=[0, 15, 30, 45],

include_lowest=True,

right=False

)

df_estate.head(5)cat_dict = {

pd.Interval(left=0, right=15, closed='left'): '0-15',

pd.Interval(left=15, right=30, closed='left'): '15-30',

pd.Interval(left=30, right=45, closed='left'): '30-45'

}

df_estate['house_age_cat_str'] = df_estate['house_age_cat'].map(cat_dict)

df_estate['house_age_cat_str'] = df_estate['house_age_cat_str'].astype('category')

df_estate.head()#Checking the updated datatype of house_age_years

df_estate.house_age_cat_str.dtypeCategoricalDtype(categories=['0-15', '15-30', '30-45'], ordered=True, categories_dtype=object)#Checking the dataframe for any NA values

df_estate.isna().any()Descriptive Statistics¶

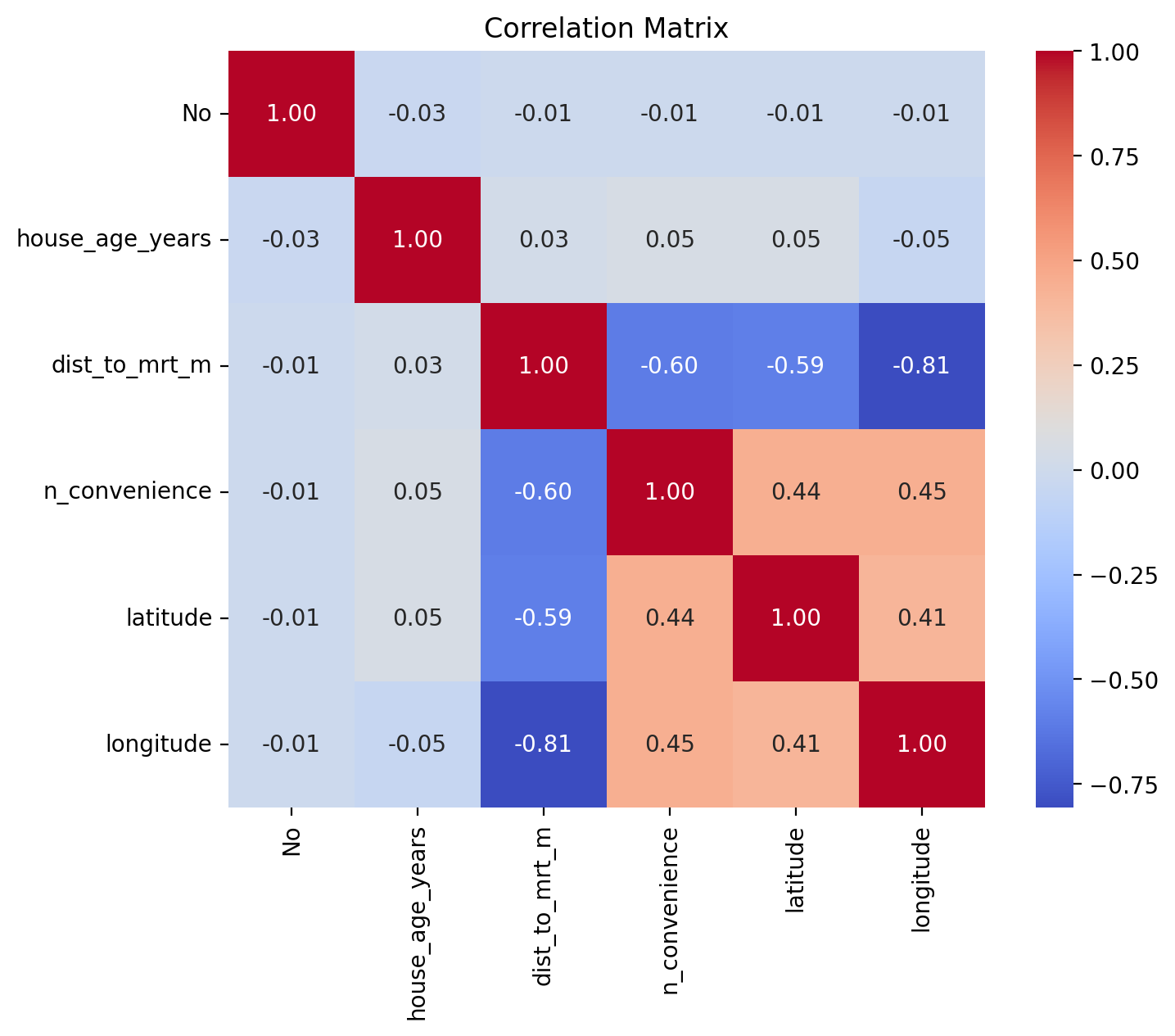

Prepare a heatmap with correlation coefficients on it:

corr_matrix = df_estate.iloc[:, :6].corr()

plt.figure(figsize=(8, 6))

sns.heatmap(corr_matrix, annot=True, fmt=".2f", cmap="coolwarm", square=True)

plt.title("Correlation Matrix")

plt.show()

Draw a scatter plot of n_convenience vs. price_twd_msq:

# Your code hereDraw a scatter plot of house_age_years vs. price_twd_msq:

# Your code hereDraw a scatter plot of distance to nearest MRT station vs. price_twd_msq:

# Your code herePlot a histogram of price_twd_msq with 10 bins, facet the plot so each house age group gets its own panel:

# Your code hereSummarize to calculate the mean, sd, median etc. house price/area by house age:

# Your code hereSimple model¶

Run a linear regression of price_twd_msq vs. best, but only 1 predictor:

import statsmodels.api as sm

# Let's use 'dist_to_mrt_m' as the single best predictor

X = df_estate[['dist_to_mrt_m']]

y = df_estate['price_twd_msq']

# Add constant for intercept

X = sm.add_constant(X)

# Fit the model

model1 = sm.OLS(y, X).fit()

# Show the summary

print(model1.summary()) OLS Regression Results

==============================================================================

Dep. Variable: price_twd_msq R-squared: 0.454

Model: OLS Adj. R-squared: 0.452

Method: Least Squares F-statistic: 342.2

Date: Sun, 25 May 2025 Prob (F-statistic): 4.64e-56

Time: 23:29:08 Log-Likelihood: -1542.5

No. Observations: 414 AIC: 3089.

Df Residuals: 412 BIC: 3097.

Df Model: 1

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

const 45.8514 0.653 70.258 0.000 44.569 47.134

dist_to_mrt_m -0.0073 0.000 -18.500 0.000 -0.008 -0.006

==============================================================================

Omnibus: 140.820 Durbin-Watson: 2.151

Prob(Omnibus): 0.000 Jarque-Bera (JB): 988.283

Skew: 1.263 Prob(JB): 2.49e-215

Kurtosis: 10.135 Cond. No. 2.19e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 2.19e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

What do the above results mean? Write down the model and interpret it.

Discuss model accuracy.

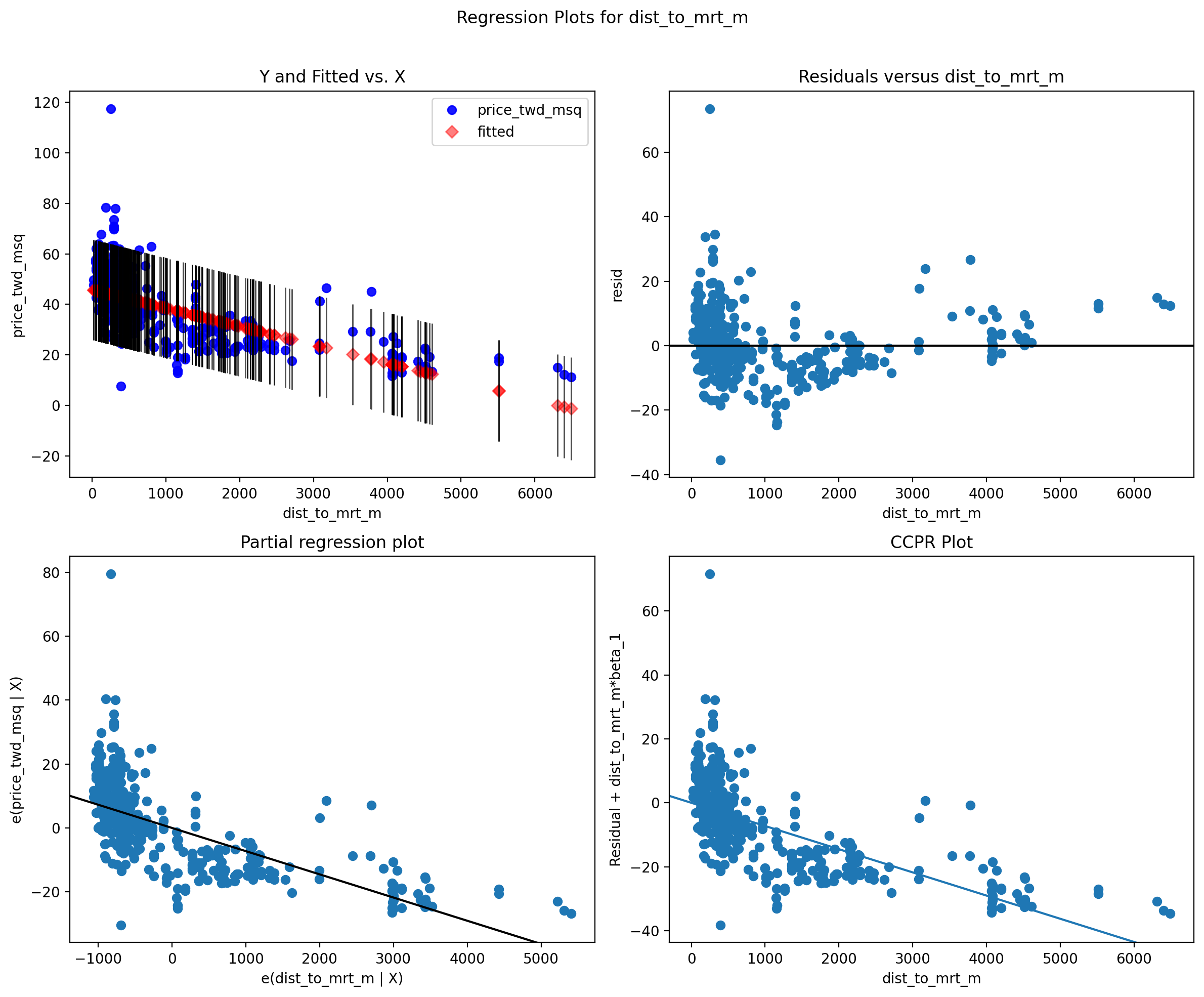

Model diagnostics¶

4 Diagnostic plots¶

fig = plt.figure(figsize=(12, 10))

sm.graphics.plot_regress_exog(model1, 'dist_to_mrt_m', fig=fig)

plt.show()

The four plots show...

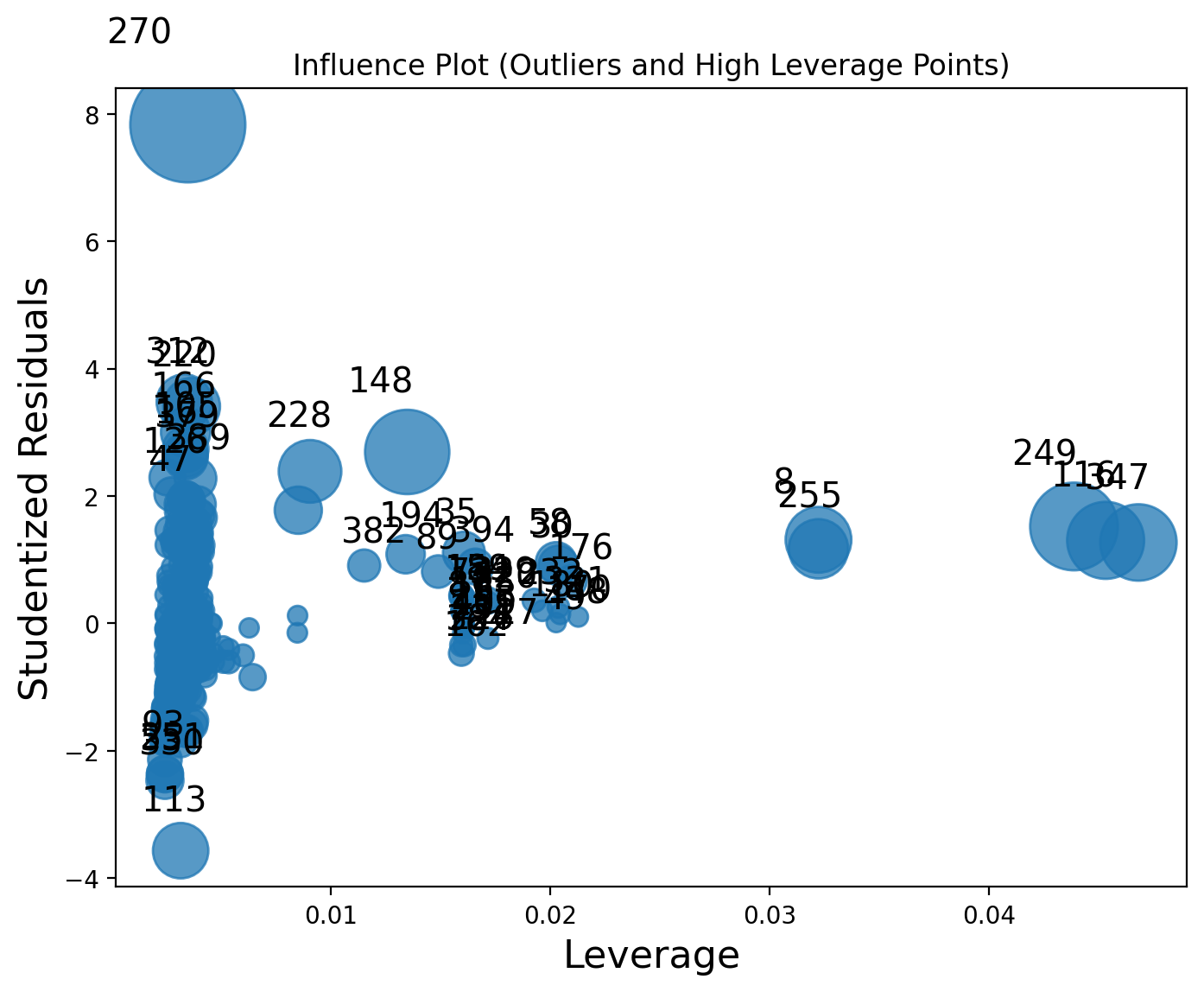

Outliers and high levarage points:¶

fig, ax = plt.subplots(figsize=(8, 6))

sm.graphics.influence_plot(model1, ax=ax, criterion="cooks")

plt.title("Influence Plot (Outliers and High Leverage Points)")

plt.show()

Discussion:

Multiple Regression Model¶

Test and training set¶

We begin by splitting the dataset into two parts, training set and testing set. In this example we will randomly take 75% row in this dataset and put it into the training set, and other 25% row in the testing set:

# One-hot encoding for house_age_cat_str in df_estate

encode_dict = {True: 1, False: 0}

house_age_0_15 = df_estate['house_age_cat_str'] == '0-15'

house_age_15_30 = df_estate['house_age_cat_str'] == '15-30'

house_age_30_45 = df_estate['house_age_cat_str'] == '30-45'

df_estate['house_age_0_15'] = house_age_0_15.map(encode_dict)

df_estate['house_age_15_30'] = house_age_15_30.map(encode_dict)

df_estate['house_age_30_45'] = house_age_30_45.map(encode_dict)

df_estate.head()from sklearn.model_selection import train_test_split

# 75% training, 25% testing, random_state=12 for reproducibility

train, test = train_test_split(df_estate, train_size=0.75, random_state=12)Now we have our training set and testing set.

Variable selection methods¶

Generally, selecting variables for linear regression is a debatable topic.

There are many methods for variable selecting, namely, forward stepwise selection, backward stepwise selection, etc, some are valid, some are heavily criticized.

I recommend this document: https://

[If our goal is prediction]{.ul}, it is safer to include all predictors in our model, removing variables without knowing the science behind it usually does more harm than good!!!

We begin to create our multiple linear regression model:

import statsmodels.formula.api as smf

model2 = smf.ols('price_twd_msq ~ dist_to_mrt_m + house_age_0_15 + house_age_30_45', data = df_estate)

result2 = model2.fit()

result2.summary()What about distance to mrt? Please plot its scatterplot with the dependent variable and verify, if any transformation is needed:

# Your code here# If any transformation is necessary, please estimate the Model3 with the transformed distance to mrt.Discuss the results...

#Calculating residual standard error of Model1

mse_result1 = model1.mse_resid

rse_result1 = np.sqrt(mse_result1)

print('The residual standard error for the above model is:',np.round(mse_result1,3))The residual standard error for the above model is: 101.375

#Calculating residual standard error of Model2

mse_result2 = result2.mse_resid

rse_result2 = np.sqrt(mse_result2)

print('The residual standard error for the above model is:',np.round(rse_result2,3))The residual standard error for the above model is: 9.796

Looking at model summary, we see that variables .... are insignificant, so let’s estimate the model without those variables:

# Estimate next model hereEvaluating multi-collinearity¶

There are many standards researchers apply for deciding whether a VIF is too large. In some domains, a VIF over 2 is worthy of suspicion. Others set the bar higher, at 5 or 10. Others still will say you shouldn’t pay attention to these at all. Ultimately, the main thing to consider is that small effects are more likely to be “drowned out” by higher VIFs, but this may just be a natural, unavoidable fact with your model.

from statsmodels.stats.outliers_influence import variance_inflation_factor

X_vif = df_estate[['dist_to_mrt_m', 'house_age_0_15', 'house_age_30_45']].copy()

X_vif = X_vif.fillna(0) # Fill missing values if any

# Add constant (intercept)

X_vif = sm.add_constant(X_vif)

# Calculate VIF for each feature

vif_data = pd.DataFrame()

vif_data["feature"] = X_vif.columns

vif_data["VIF"] = [variance_inflation_factor(X_vif.values, i) for i in range(X_vif.shape[1])]

print(vif_data) feature VIF

0 const 4.772153

1 dist_to_mrt_m 1.061497

2 house_age_0_15 1.399276

3 house_age_30_45 1.400308

Discuss the results...

Finally we test our best model on test dataset (change, if any transformation on dist_to_mrt_m was needed):

# Prepare test predictors (must match training predictors)

X_test = test[['dist_to_mrt_m', 'house_age_0_15', 'house_age_30_45']].copy()

X_test = X_test.fillna(0)

X_test = sm.add_constant(X_test)

# True values

y_test = test['price_twd_msq']

# Predict using model2

y_pred = result2.predict(X_test)

# Calculate RMSE as an example metric

from sklearn.metrics import mean_squared_error

rmse = np.sqrt(mean_squared_error(y_test, y_pred))

print(f"Test RMSE: {rmse:.2f}")Test RMSE: 8.38

Interpret results...

Variable selection using best subset regression¶

Best subset and stepwise (forward, backward, both) techniques of variable selection can be used to come up with the best linear regression model for the dependent variable medv.

# Best subset selection using sklearn's SequentialFeatureSelector (forward and backward)

from sklearn.feature_selection import SequentialFeatureSelector

from sklearn.linear_model import LinearRegression

# Prepare predictors and target

X = df_estate[['dist_to_mrt_m', 'n_convenience', 'house_age_0_15', 'house_age_15_30', 'house_age_30_45']]

y = df_estate['price_twd_msq']

# Initialize linear regression model

lr = LinearRegression()

# Forward stepwise selection

sfs_forward = SequentialFeatureSelector(lr, n_features_to_select='auto', direction='forward', cv=5)

sfs_forward.fit(X, y)

print("Forward selection support:", sfs_forward.get_support())

print("Selected features (forward):", X.columns[sfs_forward.get_support()].tolist())

# Backward stepwise selection

sfs_backward = SequentialFeatureSelector(lr, n_features_to_select='auto', direction='backward', cv=5)

sfs_backward.fit(X, y)

print("Backward selection support:", sfs_backward.get_support())

print("Selected features (backward):", X.columns[sfs_backward.get_support()].tolist())Forward selection support: [ True True False False False]

Selected features (forward): ['dist_to_mrt_m', 'n_convenience']

Backward selection support: [ True True False False True]

Selected features (backward): ['dist_to_mrt_m', 'n_convenience', 'house_age_30_45']

Comparing competing models¶

import statsmodels.api as sm

# Example: Compare AIC for models selected by forward and backward stepwise selection

# Forward selection model

features_forward = X.columns[sfs_forward.get_support()].tolist()

X_forward = df_estate[features_forward]

X_forward = sm.add_constant(X_forward)

model_forward = sm.OLS(y, X_forward).fit()

print("AIC (forward selection):", model_forward.aic)

# Backward selection model

features_backward = X.columns[sfs_backward.get_support()].tolist()

X_backward = df_estate[features_backward]

X_backward = sm.add_constant(X_backward)

model_backward = sm.OLS(y, X_backward).fit()

print("AIC (backward selection):", model_backward.aic)

# You can print summary for the best model (e.g., forward)

print(model_forward.summary())AIC (forward selection): 3057.2813425866216

AIC (backward selection): 3047.991777087278

OLS Regression Results

==============================================================================

Dep. Variable: price_twd_msq R-squared: 0.497

Model: OLS Adj. R-squared: 0.494

Method: Least Squares F-statistic: 202.7

Date: Sun, 25 May 2025 Prob (F-statistic): 5.61e-62

Time: 23:43:56 Log-Likelihood: -1525.6

No. Observations: 414 AIC: 3057.

Df Residuals: 411 BIC: 3069.

Df Model: 2

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

const 39.1229 1.300 30.106 0.000 36.568 41.677

dist_to_mrt_m -0.0056 0.000 -11.799 0.000 -0.007 -0.005

n_convenience 1.1976 0.203 5.912 0.000 0.799 1.596

==============================================================================

Omnibus: 191.943 Durbin-Watson: 2.126

Prob(Omnibus): 0.000 Jarque-Bera (JB): 2159.977

Skew: 1.671 Prob(JB): 0.00

Kurtosis: 13.679 Cond. No. 4.58e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 4.58e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

From Best subset regression and stepwise selection (forward, backward, both), we see that the models selected by forward and backward selection may include different sets of predictors, depending on their contribution to model fit.

By comparing AIC values, the model with the lowest AIC is preferred, as it balances model complexity and goodness of fit.

In this case, the summary output for the best model (e.g., forward selection) shows which variables are most important for predicting price_twd_msq. This approach helps identify the most relevant predictors and avoid overfitting by excluding unnecessary variables.

Run model diagnostics for the BEST model:

# Your code hereFinally, we can check the Out-of-sample Prediction or test error (MSPE):

X_test = test[features_forward].copy()

X_test = X_test.fillna(0)

X_test = sm.add_constant(X_test)

# True values

y_test = test['price_twd_msq']

# Predict using the best model (e.g., forward selection)

y_pred = model_forward.predict(X_test)

# Calculate MSPE (Mean Squared Prediction Error)

mspe = np.mean((y_test - y_pred) ** 2)

print(f"Test MSPE (out-of-sample): {mspe:.2f}")Test MSPE (out-of-sample): 64.80

Cross Validation¶

In Python, for cross-validation of regression models is usually done with cross_val_score from sklearn.model_selection.

To get the raw cross-validation estimate of prediction error (e.g., mean squared error), use:

from sklearn.model_selection import cross_val_score

from sklearn.linear_model import LinearRegression

X = df_estate[['dist_to_mrt_m', 'house_age_0_15', 'house_age_30_45']]

y = df_estate['price_twd_msq']

model = LinearRegression()

# 5-fold cross-validation, scoring negative MSE (so we multiply by -1 to get positive MSE)

cv_scores = cross_val_score(model, X, y, cv=5, scoring='neg_mean_squared_error')

# Raw cross-validation estimate of prediction error (mean MSE)

cv_mse = -cv_scores.mean()

cv_rmse = np.sqrt(cv_mse)

print(f"Cross-validated MSE: {cv_mse:.2f}")

print(f"Cross-validated RMSE: {cv_rmse:.2f}")Cross-validated MSE: 95.90

Cross-validated RMSE: 9.79

Summary¶

Do you understand all numerical measures printed in the SUMMARY of the regression report?

Why do we need a cross-validation?

What are the diagnostic plots telling us?

How to compare similar, but competing models?

What is VIF telling us?

How to choose best set of predictors for the model?